DeFi pulse is an Ethereum lending TVL lens for Maker and Aave

In short: DeFi analytics dashboard tracking Ethereum lending TVL, with Maker and Aave views for comparing protocol deposits over time.

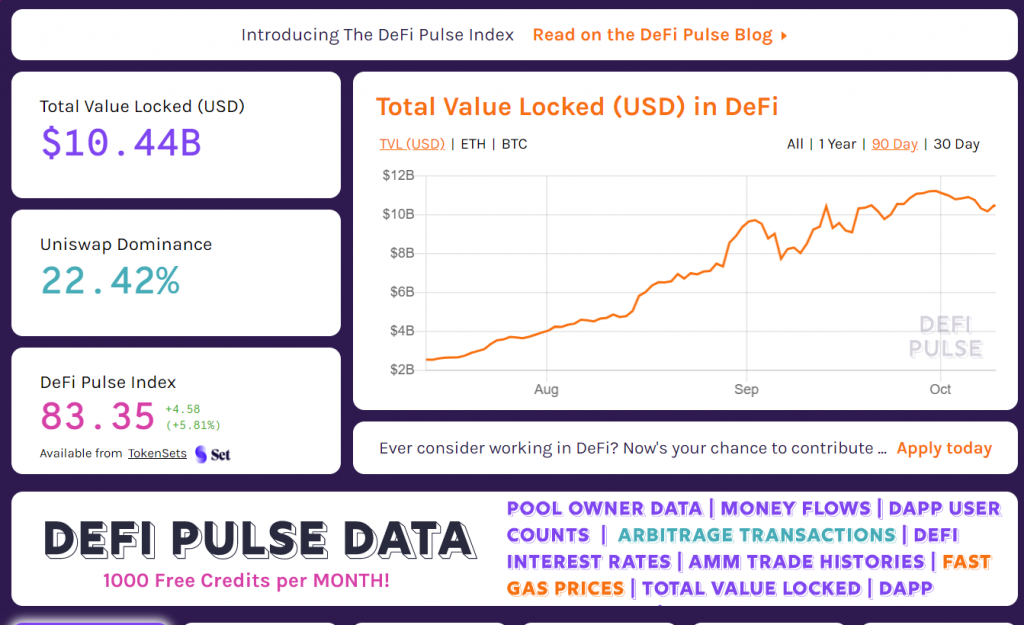

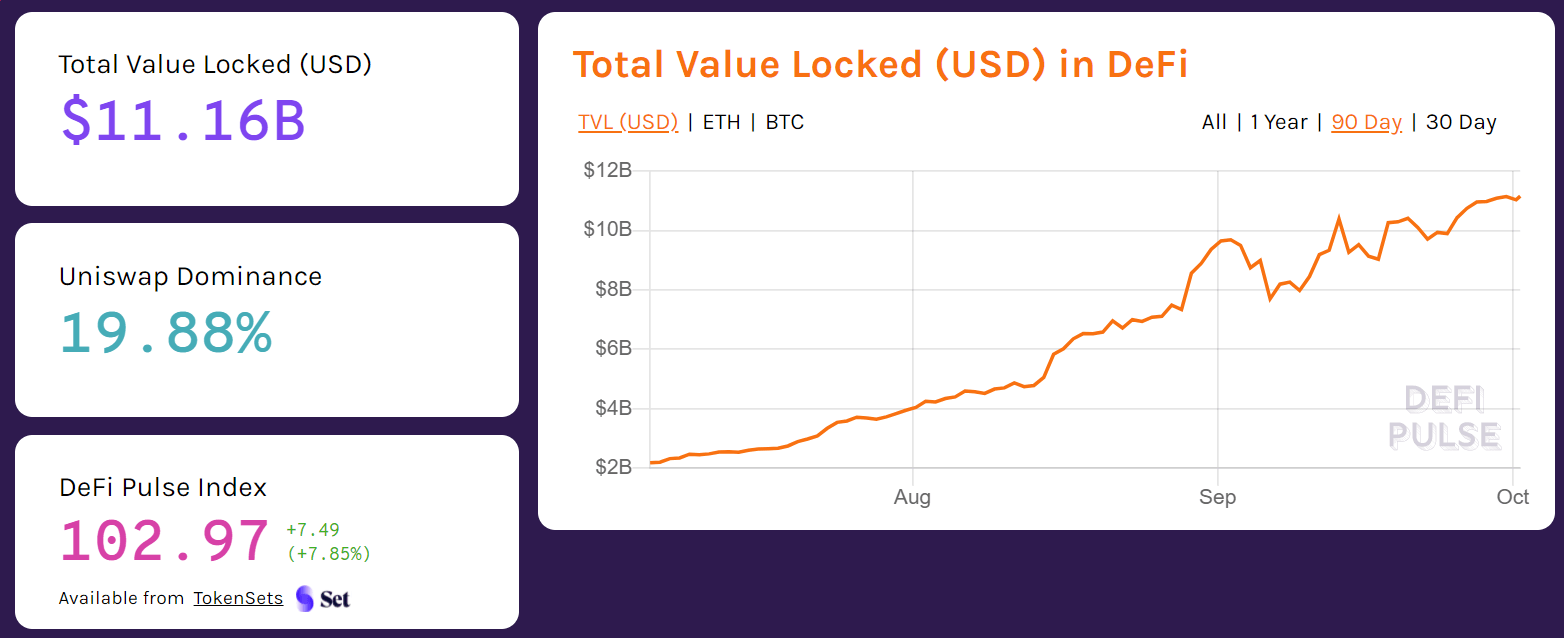

Defi pulse is an Ethereum lending TVL lens for reading how much crypto value is deposited in protocols such as Maker and Aave. Its main use is straightforward: it turns on-chain lending activity into comparable totals, charts, and protocol rankings, so a reader sees whether liquidity is moving into collateralized debt markets, pooled lending markets, or the wider DeFi economy.

The page is best understood as a research view rather than a trading terminal. It organizes total value locked, a metric that counts the market value of assets committed to smart contracts, and places lending protocols beside one another. Maker, Aave, and similar systems do different things under the hood, yet TVL gives analysts a common yardstick for capital depth, user confidence, and liquidity concentration.

Reading Maker and Aave through lending TVL

Maker and Aave represent two different shapes of Ethereum lending. MakerDAO centers on overcollateralized DAI creation: users lock accepted collateral, generate DAI debt, and manage liquidation risk through vault parameters. Aave uses pooled markets: suppliers deposit assets, borrowers draw from liquidity pools, and interest rates move according to utilization.

Defi pulse gives these models a shared frame by focusing on deposited value. A large Maker total signals substantial collateral backing DAI positions. A large Aave total signals deep pooled liquidity across assets such as ETH, stablecoins, and wrapped tokens. The numbers do not describe profit by themselves, but they show where capital has chosen to sit.

How total value locked becomes a usable signal

TVL begins with balances. A lending protocol holds collateral, supplied assets, or liquidity inside smart contracts. Those balances are priced in a reference currency and added into a protocol-level total. The same idea extends to category rankings, where lending, decentralized exchanges, derivatives, and asset management protocols are grouped by the capital committed to them.

Day to day, Defi pulse became associated with this style of dashboard because it made a complex on-chain environment legible. The useful part is comparison over time: a one-day number matters less than the slope, the drawdown, and the recovery after stress. Rising TVL shows more assets entering a protocol; falling TVL shows withdrawals, price declines in deposited collateral, or both.

Where lending TVL helps during market stress

Sharp market moves expose the difference between price charts and lending dashboards. When ETH or other collateral drops, Maker vaults face lower collateral ratios and Aave borrowers move closer to liquidation thresholds. A TVL chart will reflect the market value decline immediately, even before users add collateral, repay debt, or withdraw funds.

This makes Defi pulse useful for studying risk cycles. If lending TVL falls across Maker, Aave, and Compound at the same time, the move points to broad deleveraging or collateral repricing. If one protocol loses value faster than the category, the cause is worth investigating: asset mix, liquidation design, governance changes, incentive shifts, or a temporary migration to another venue.

Maker data needs context beyond the headline total

Maker's TVL is tied to collateral supporting DAI. A high total suggests meaningful backing inside the system, but the composition matters. ETH collateral behaves differently from tokenized real-world assets, stablecoin collateral, or liquid staking tokens. Debt ceilings, stability fees, liquidation ratios, and oracle updates shape how users interact with vaults.

When Defi pulse places Maker in a lending table, the clean ranking hides those internal differences. A reader should treat Maker's line as a starting measurement for collateral depth, then connect it to DAI supply, vault risk parameters, and governance decisions. That second layer explains whether deposited value is concentrated in a few collateral types or spread across a broader risk base.

Aave deposits show liquidity depth across markets

Aave TVL reflects supplied liquidity across its supported assets and deployments. On Ethereum, users deposit tokens into pools and receive interest-bearing receipt tokens that track their supplied position. Borrowers pay rates shaped by utilization, and liquidations protect the pool when collateral values fall below required thresholds.

Importantly, Defi pulse makes Aave easier to compare with Maker because both appear under a capital-committed lens. Still, the interpretation differs. Aave's deposited value speaks to available borrow liquidity and market depth. Maker's deposited value speaks to collateral locked against DAI debt. The same TVL unit covers two separate lending designs.

Getting a clean read before comparing protocols

A useful lending review starts with a few fixed questions. The goal is to separate protocol adoption from token price movement, incentive campaigns, and temporary liquidity shifts. A dashboard answer becomes stronger when it is paired with the mechanism that created the number.

- Check whether TVL moved because deposited token prices changed.

- Compare the protocol line with the broader lending category.

- Look for simultaneous moves in DAI supply, borrow demand, or stablecoin liquidity.

- Separate Ethereum mainnet activity from activity on other networks.

- Watch liquidation periods, governance votes, and collateral parameter changes.

This approach keeps Defi pulse from becoming a raw scoreboard. The ranking is useful, but the story sits in the interaction between deposits, debt, prices, and protocol rules.

Benefits for analysts, builders, and protocol researchers

Analysts use TVL because it turns fragmented smart contract balances into a common metric. Builders study it to understand which designs attract durable liquidity. Protocol researchers use lending rankings to see how collateralized debt markets, pooled borrowing, and stablecoin systems react under pressure.

In practice, Defi pulse also helps explain DeFi to people who already understand market capitalization but need a better measure for protocol usage. Market cap prices a token. TVL measures assets placed into contracts. The two figures answer different questions, and lending dashboards highlight that difference clearly.

Limits that matter when using the dashboard

TVL is powerful, but it is not a complete health score. A protocol with high deposits still needs sound oracle design, liquidation incentives, governance discipline, audited contracts, and resilient liquidity during volatility. A smaller protocol with conservative collateral rules might carry less systemic risk than a larger one with crowded positions.

The most important caution is methodological: TVL depends on pricing, contract selection, and how repeated or wrapped assets are counted. Defi pulse gives a practical view of Ethereum lending liquidity, yet serious analysis also checks protocol documentation, on-chain positions, risk parameters, and current governance activity before drawing conclusions.

Before you start with Defi pulse

Which Maker metrics pair best with a lending TVL chart?

Maker TVL makes more sense when it is viewed beside DAI supply, collateral composition, stability fees, liquidation ratios, and debt ceilings. Those details explain whether the locked value supports broad, diversified DAI creation or concentrates around a few collateral types. A TVL increase backed by one volatile asset tells a different story from growth spread across ETH, stablecoins, and other approved collateral.

Does Aave TVL include borrowed assets or supplied assets?

Aave TVL is centered on assets supplied to its liquidity pools, priced and aggregated into a protocol total. Borrowing activity matters because utilization affects interest rates, but the visible locked-value figure primarily reflects deposited liquidity. To understand the lending market fully, compare supplied liquidity with outstanding borrows, reserve factors, asset caps, and liquidation activity.

Can lending TVL fall while user deposits stay the same?

Yes. If the market price of deposited collateral drops, the dollar value of TVL falls even when token balances inside contracts remain unchanged. This is common when ETH, wrapped Bitcoin, or other volatile collateral reprices quickly. That is why a serious reading separates balance changes from price changes before treating a decline as user withdrawals.

Do I need a wallet to use a DeFi lending analytics dashboard?

A wallet is not required for reading public lending analytics. Dashboards display aggregated protocol data drawn from smart contracts, indexers, and pricing feeds, so a visitor can study Maker, Aave, and other markets without connecting an address. A wallet becomes relevant only when the user moves from research into direct protocol interaction.

Why do Maker and Aave show different TVL behavior during volatility?

Their lending designs respond to stress differently. Maker positions revolve around collateral locked against DAI debt, so vault repayments, collateral additions, and liquidations change the picture. Aave uses pooled lending, where suppliers, borrowers, utilization, and asset caps shape liquidity. During volatility, these mechanics create different deposit flows even when both protocols operate on Ethereum.

When is a TVL ranking misleading for Ethereum lending?

A ranking becomes misleading when it is read without asset composition, leverage, and pricing context. A protocol can rise because a deposited token appreciated, because incentives attracted short-term deposits, or because wrapped assets were counted in a way that inflates apparent liquidity. The ranking is most useful when paired with borrow demand, collateral rules, and recent governance changes.